The Short Answer: Debt recovery lawyers help financial institutions collect unpaid debt while following federal law and state regulations. Working with a qualified debt collection lawyer reduces your legal exposure, improves recovery rates, and keeps your organization compliant with the Fair Debt Collection Practices Act (FDCPA) and Regulation F.

For banks, credit unions, and other creditors across the United States, recovering outstanding debt is part of doing business. But the rules around how a debt collector can pursue payment have grown more detailed, and 2026 brings a unique challenge: the Consumer Financial Protection Bureau (CFPB) has scaled back its enforcement activity, and state attorneys general are stepping in to fill the gap. This guide breaks down the laws that govern debt recovery, the most common compliance mistakes, and when it makes sense to bring in outside legal counsel.

The Regulatory Landscape for Debt Recovery in 2026

Financial institutions and the attorneys or agencies representing them must follow a layered set of rules when collecting debt. Here is what you need to know in 2026.

The Fair Debt Collection Practices Act (FDCPA)

The FDCPA remains the foundation of debt collection regulation at the federal level. It governs how a third-party debt collector can communicate with consumers and what practices are off-limits. Under the FDCPA, a collector cannot contact consumers before 8 a.m. or after 9 p.m. without prior consent, use threats of violence, make misleading statements about the amount owed, or use unconscionable means to pressure payment. The law also restricts what a debt collector can say to third parties. For example, a collector may contact someone other than the debtor only to obtain location information such as the debtor’s address or phone number, and even then, the collector generally cannot reveal that a debt is owed.

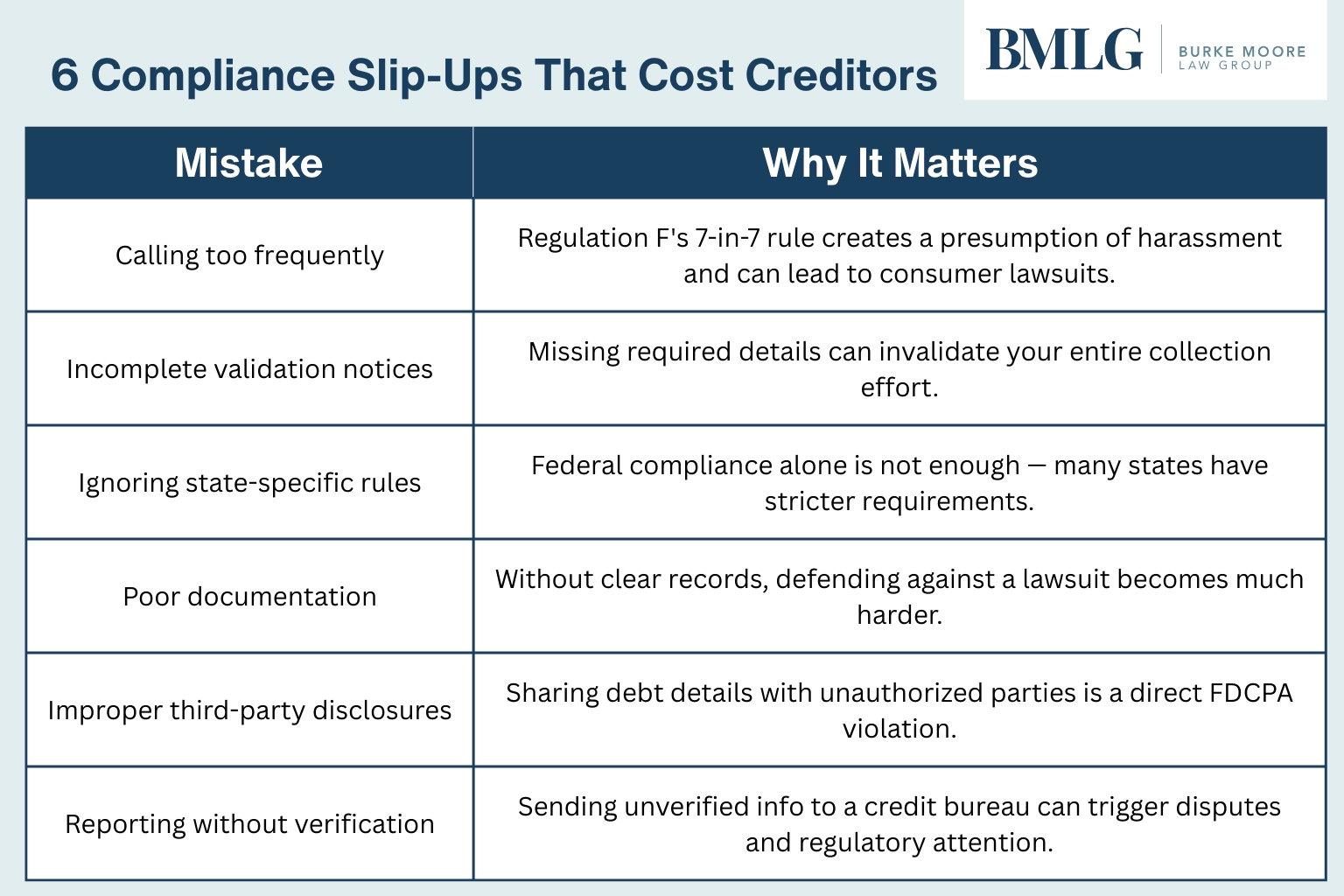

One important distinction: the FDCPA applies to third-party debt collectors and collection agencies, not to the original creditor collecting its own accounts. However, many states extend similar protections to original creditor activity. Both the Federal Trade Commission (FTC) and the CFPB have authority to enforce unfair debt collection practice claims under federal law.

Regulation F

Regulation F, which took effect in November 2021, is the CFPB’s modern interpretation of the FDCPA. It introduced rules around digital communication methods (including email, text, and social media), placed limits on call frequency, and standardized the validation notice format that a debt collector must send to consumers.

Under Regulation F, a collector is generally presumed to violate the law if they place more than seven calls within seven consecutive days about a particular debt, or call within seven days after having a phone conversation about that debt. The rule also requires that a validation notice include the debt amount, the creditor’s name, an itemization of the current balance, and a clear explanation of the consumer’s right to dispute. Sending this notice by certified mail with a return receipt requested can provide useful documentation, though it is not required.

State-Level Rules and the 2026 Enforcement Shift

On top of federal law, most states have their own debt collection statutes. Some have stricter communication restrictions, shorter statutes of limitations, or additional licensing requirements for any collection agency operating within their borders. New York, for instance, requires specific disclosures for consumer debts and offers multilingual resources. California’s Rosenthal Act extends FDCPA-like protections to original creditors. In certain states, specific collection violations can be classified as a criminal offense, not just a civil matter.

What makes 2026 different is the enforcement landscape. The CFPB has significantly reduced its supervisory activity, with staffing cuts and a narrowed focus. In response, state attorneys general have stepped up their own consumer financial protection efforts, particularly around debt collection. The practical takeaway is clear: compliance now requires attention to both federal rules and an increasingly active patchwork of state-level enforcement. Working with debt recovery lawyers who are licensed in every state where you operate is the most reliable way to manage that complexity.

Common Compliance Mistakes Financial Institutions Make

Even well-run organizations can run into trouble if their collection process has gaps. Below are the most frequent mistakes and why they create risk.

When a Debt Collection Lawyer Makes Sense

Many financial institutions manage early-stage collection efforts in-house. But there are clear points where bringing in a debt collection lawyer adds real value.

Accounts Past Internal Collections

If a delinquent debt has been unresponsive for 90 or more days and your internal team has followed its standard process, a law firm can step in with legal demand letters and, if needed, file court papers to pursue the balance. A formal letter from an attorney often prompts payment from consumers who have stopped responding to a debt collection agency or internal outreach team. If the debtor still does not respond, the firm can seek a default judgment on your behalf.

Multi-State or High-Volume Portfolios

If your institution holds credit card, auto loan, or other consumer debt across multiple states, keeping up with each state’s rules is a serious challenge. A national debt recovery law firm with licensed attorneys in the relevant jurisdictions can handle filings, court appearances, and negotiations without outsourcing to unfamiliar local counsel.

Bankruptcy and Post-Judgment Recovery

When a debtor files for bankruptcy, the rules around what a creditor can do change immediately. Debt recovery lawyers experienced in bankruptcy proceedings can file proofs of claim, attend hearings, and protect your institution’s interests. Post-judgment work, such as garnishments against a bank account, liens, and asset discovery, also requires legal assistance to execute properly.

What to Look for in a Collections Law Firm

Not every firm that handles debt will be the right fit. A debt collection agency and a collections law firm serve different roles. A law firm can litigate, appear in court, and provide legal counsel, while a collection agency typically handles pre-legal outreach. Here is what to look for in a legal partner.

- A strong compliance program: Look for a firm with a dedicated compliance team, internal quality monitoring, and a clear process for tracking regulatory changes at both the federal and state level.

- National reach with local expertise: A firm with attorneys licensed in the states where you do business can handle filings and hearings without subcontracting to outside counsel. This is especially important for collecting legitimate debt across multiple jurisdictions.

- Technology and process discipline: Firms that use modern case management and reporting tools can move faster, document collection efforts more thoroughly, and give you real-time visibility into your portfolio.

- Respectful debtor engagement: How a collector treats consumers reflects directly on your institution. Choose a partner that communicates respectfully and offers resolution options like a payment plan when appropriate.

- Extensive industry experience: A firm with a track record serving banks, credit unions, and financial services companies will understand the specific debt recovery challenges your institution faces.

How Compliance Protects Your Bottom Line

Compliance and recovery are not at odds. Financial institutions that follow collection rules closely tend to recover more over time, for a few practical reasons.

First, compliant practices lead to fewer consumer complaints and lawsuits. FDCPA violations can result in statutory damages of up to $1,000 per legal action, plus attorney fees. In class actions, that number can climb to $500,000 or 1% of the debt collector’s net worth, along with court costs.

Second, transparent communication with consumers produces better payment outcomes. People are more likely to settle an outstanding debt or agree to a payment arrangement when they feel treated fairly.

Third, a clean compliance record protects your institution’s reputation. In a year where state attorneys general are watching the debt collection space more closely than ever, partnering with a firm that shares your commitment to professionalism sends a strong signal to regulators and customers alike.

Moving Forward

Compliant debt recovery does not have to be complicated, but it does require the right legal partner. With federal enforcement shifting and state-level oversight increasing, 2026 is a year where the details matter. If your organization is looking for experienced debt recovery lawyers who understand the legal landscape and the importance of respectful debtor engagement, Burke Moore Law Group can help. With a team of more than 30 attorneys serving clients nationwide, Burke Moore delivers results through a compliance-first approach to debt collection and claims recovery. Contact Burke Moore Law Group at 1-877-219-5222 or visit burkemoore.com to get started.