The Short Answer: Bankruptcy creditors’ rights are the legal protections that allow lenders, financial institutions, and businesses to recover money from a debtor who has filed for bankruptcy protection. These rights are governed by the bankruptcy code and require fast action, careful documentation, and experienced creditors’ rights counsel.

When a debtor files for bankruptcy, creditors face strict deadlines, federal court procedures, and complex priority rules under the bankruptcy code. The bankruptcy process is technical, but creditors have rights to recover what they are owed. The challenge is knowing which actions to take, when to take them, and how to protect your position throughout the bankruptcy case. This guide covers how creditors’ rights work, what tools are available to recover funds, and how a strong creditors’ rights practice protects recovery when timing and procedure matter most.

What Are Bankruptcy Creditors’ Rights?

Bankruptcy creditors’ rights are the legal protections that allow a creditor to participate in a bankruptcy proceeding and recover money owed to them. These rights are spelled out in the U.S. bankruptcy code and applied through federal courts known as bankruptcy courts.

Who Qualifies as a Creditor?

A creditor is any party owed money by the debtor at the time of the bankruptcy filing. This includes:

- Financial institutions like banks, credit unions, and hedge funds

- Insurance companies

- Commercial businesses owed money on accounts receivable

- Landlords owed rent

- Vendors owed for goods or services delivered

- Holders of mortgages, equipment loans, or other secured debt

Secured vs. Unsecured Creditors

The bankruptcy code treats creditors differently based on whether their claim is backed by collateral.

| Creditor Type | What It Means | Recovery Priority |

| Secured creditor | Holds collateral or a perfected security interest (real estate, equipment, vehicles) | Highest priority against that collateral |

| Unsecured creditor | No collateral backing the debt | Recovers after secured and priority claims are paid |

| Priority unsecured creditor | Certain claims given priority by statute (taxes, wages) | Higher priority than general unsecured creditors |

The Bankruptcy Process and Where Creditors Fit In

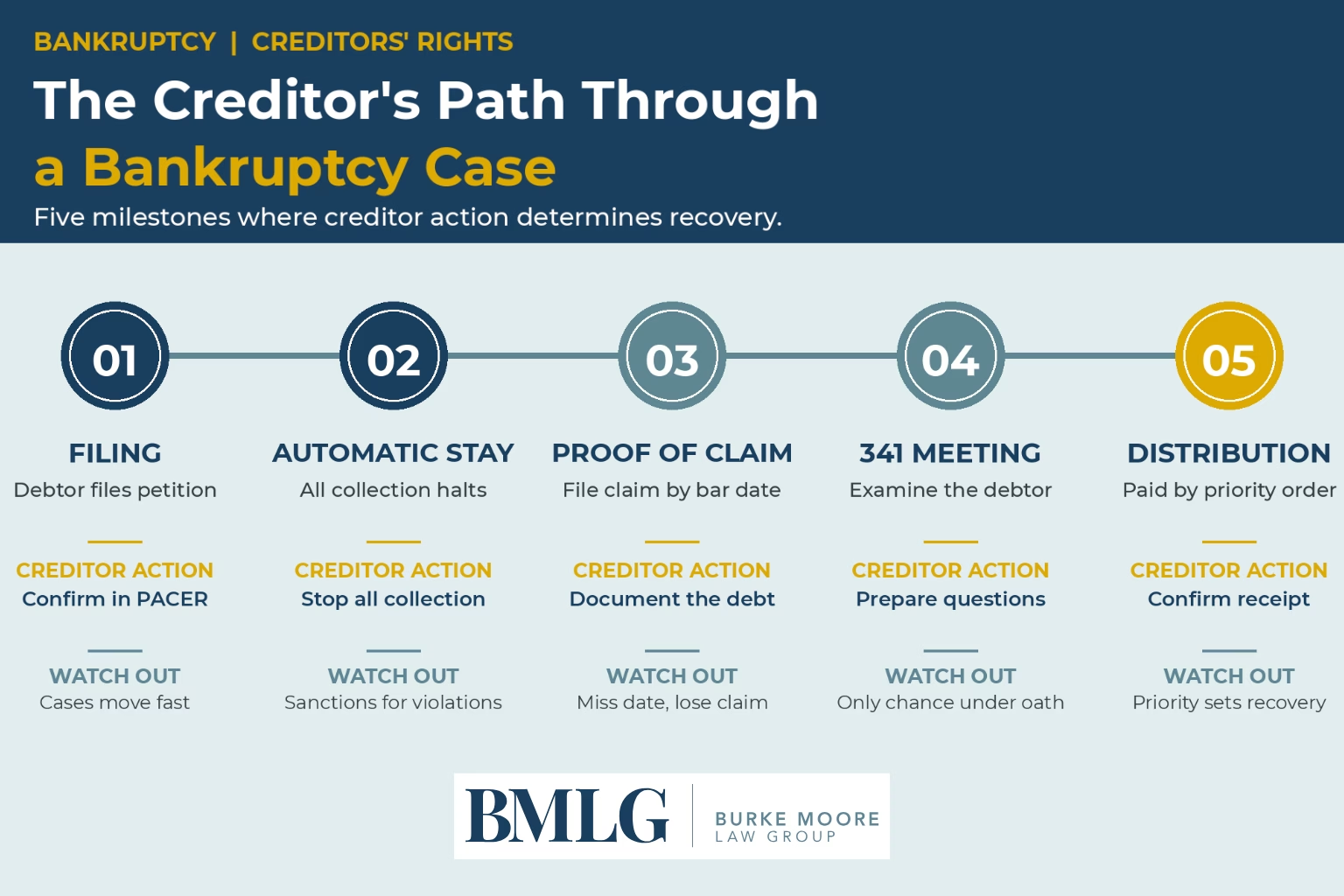

The Automatic Stay

The moment a debtor files for bankruptcy, an automatic stay takes effect. This stops all collection activity, including phone calls, lawsuits, and judgment enforcement. Creditors who violate the automatic stay face penalties from the bankruptcy court, so the first call after a bankruptcy filing should be to a qualified creditors’ rights attorney.

Filing a Proof of Claim

A proof of claim is the document a creditor files to assert their right to be paid from the bankruptcy estate. Deadlines are strict, and a missed deadline can mean the claim is disallowed entirely. The proof of claim should include:

- The amount owed

- Documentation supporting the debt

- Evidence of any security interest

- Records of payments received

The Meeting of Creditors

Also called the 341 meeting, this is where creditors can question the debtor under oath. It is a chance to examine claims of inability to pay, ask about transferred assets, and gather information for later litigation if needed.

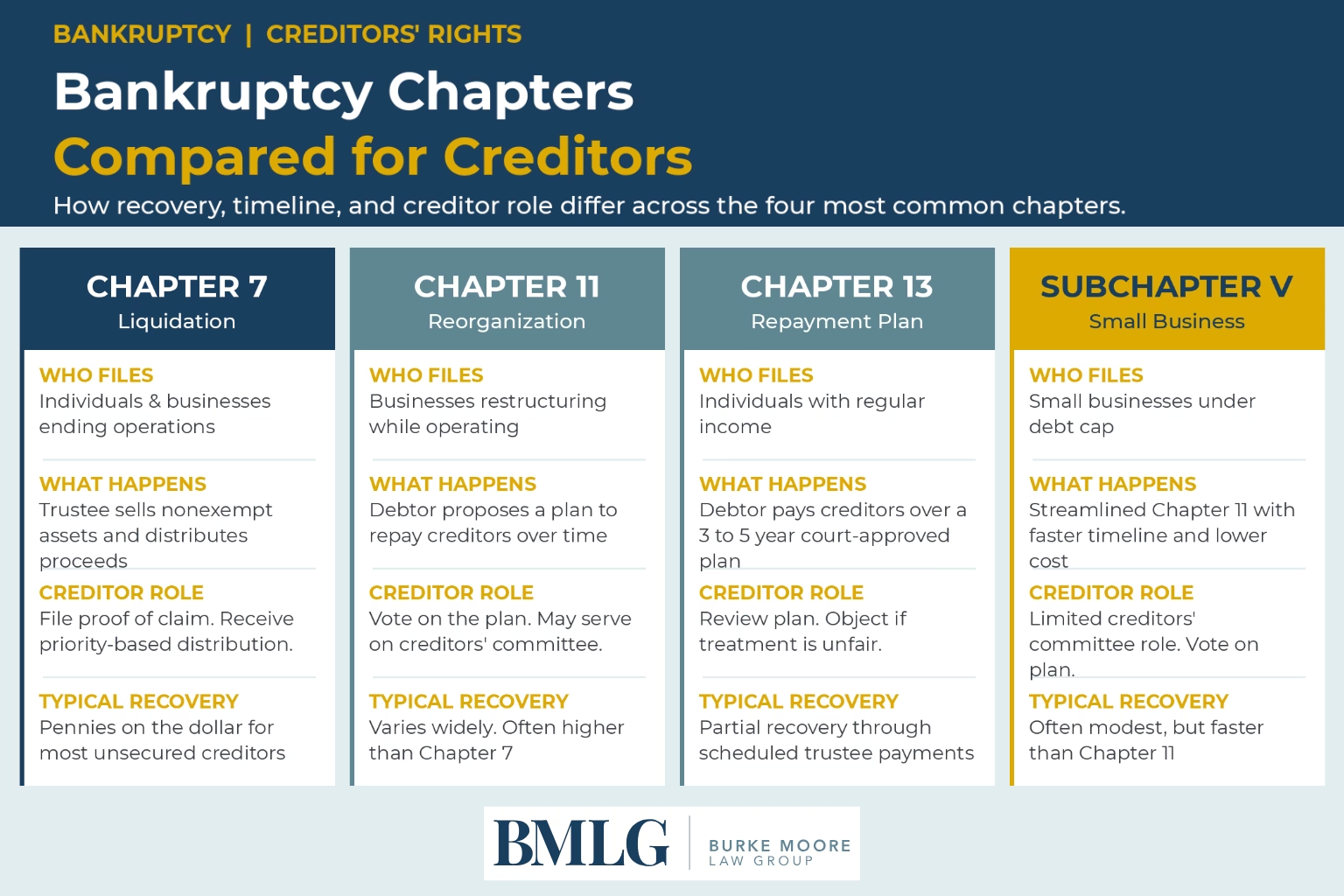

How Creditors Recover in Different Types of Bankruptcy

The recovery path depends on which chapter of the bankruptcy code the debtor filed under.

Chapter 7: Liquidation

In a Chapter 7 case, the debtor’s nonexempt assets are sold by the Chapter 7 trustee and the proceeds are distributed to creditors based on priority. Secured creditors recover against their collateral first. Unsecured creditors share what remains, often receiving cents on the dollar or nothing at all.

Chapter 11: Reorganization

Chapter 11 cases allow the debtor (often a business) to reorganize debts while continuing to operate. Creditors negotiate the proposed plan, vote on whether to accept it, and may serve on

creditors’ committees. Lead counsel with bankruptcy practice experience often handles these negotiations.

Subchapter V: Small Business Cases

An expedited Chapter 11 process for small businesses, Subchapter V cases move faster and reduce the role of creditors’ committees, which changes how creditors negotiate their position.

Chapter 13: Repayment Plans

Chapter 13 lets individual debtors keep their property and pay creditors over three to five years through a court-approved repayment plan. Creditors review the plan, object if treatment is unfair, and receive payments through the bankruptcy trustee.

Legal Tools Creditors Use to Protect Their Rights

Beyond filing a proof of claim, creditors have several legal tools available during a bankruptcy proceeding.

Adversary Proceedings

An adversary proceeding is a lawsuit filed within a bankruptcy case. Common types include:

- Nondischargeability actions: asking the court to rule that a debt cannot be wiped out, often based on fraud or willful and malicious injury

- Lien validity challenges: disputes over whether a security interest was properly perfected under the uniform commercial code

- Preference actions and fraudulent transfer litigation: brought to recover payments or transfers the debtor made before filing

Avoidance Actions

A bankruptcy trustee or debtor-in-possession can bring avoidance actions against creditors to recover certain pre-bankruptcy transfers. Experienced creditors anticipate these claims, document defenses early, and litigate when needed.

Lender Liability Actions

Borrowers sometimes file lender liability actions against creditors, claiming the lender breached a fiduciary duty or duty of good faith. Creditors with the right counsel can defeat these claims through summary judgment or aggressive defense work.

Out-of-Court Workouts and Loan Workouts

Sometimes the better path is to resolve the matter outside of bankruptcy entirely. Out-of-court workouts and loan workouts let creditors and debtors restructure debt through corporate restructuring agreements that avoid the time and cost of full bankruptcy litigation. Alternative paths like asset purchasers stepping in to buy distressed loans can also produce better recoveries than waiting for the bankruptcy process to run its course.

Common Mistakes Creditors Make in Bankruptcy

Even experienced creditors lose recovery dollars by making preventable mistakes.

- Missing the proof of claim deadline. The bar date is firm and rarely extended, and a late filing usually disallows the claim.

- Ignoring the automatic stay. Continuing collection activity can lead to sanctions.

- Failing to monitor the case. Plan confirmations, asset sales, and adversary proceedings all happen on tight timelines.

- Skipping the meeting of creditors. This gives up your right to examine the debtor under oath.

- Not perfecting security interests before filing. Unperfected liens get treated as unsecured claims, dropping the creditor’s priority.

- Going it alone. Bankruptcy litigation in federal courts is technical and unforgiving. Bankruptcy attorneys with experience routinely recover amounts that pro se creditors miss.

Why Working With Experienced Creditors’ Rights Attorneys Matters

An effective creditors’ rights practice combines bankruptcy code knowledge with practical solutions tailored to each client’s portfolio.

What to Look For in Counsel

- Experience handling adversary proceedings, fraudulent transfer litigation, and preference actions

- Litigation experience across federal courts and bankruptcy courts nationwide

- Working knowledge of the uniform commercial code, public finance principles, and intellectual property collateral issues when relevant

- A track record representing financial institutions, insurance companies, and other commercial clients

- Industry recognition in the bankruptcy field

- Documented attorney-client relationship protocols and clear billing practices

The Pre-Legal and Legal Advantage

Some firms only handle pre-legal recovery. Others only litigate. The best creditors’ rights attorneys handle both, eliminating handoffs and giving creditors a single point of accountability from initial demand through final recovery.

Take Action to Protect Your Creditors’ Rights

Bankruptcy creditors’ rights give lenders, financial institutions, and businesses tools to recover money when a debtor files for bankruptcy protection, but those rights only work when creditors act quickly and with the right legal support. Missing deadlines, ignoring procedural rules, or trying to handle bankruptcy litigation alone usually means leaving recovery on the table.

Burke Moore Law Group is an Atlanta-based boutique law firm with more than 30 attorneys representing banks, credit unions, hedge funds, insurance companies, and commercial businesses in bankruptcy, debt collection, foreclosure, SBA collection, and general liability and defense matters nationwide. Contact us to discuss a recovery strategy led by experienced bankruptcy counsel.