The Short Answer: AI policies for law firms are tightening fast, and debt collection sits in the middle of that shift. Creditors seeking clean, compliant recovery results should confirm their counsel uses AI tools under attorney oversight rather than as a replacement for legal decision-making. Law firms must provide clear guidance on how AI tools are implemented in their processes so they follow both legal standards and ethical guidelines.

AI is no longer experimental in the legal profession. Law firms are using artificial intelligence for legal research, document review, and account workflows. As these technological advancements continue, bar associations are responding with formal ethical guidance. For creditors, that shift has direct implications for how outstanding debts are managed, recovered, and litigated. Understanding how AI policies for law firms are evolving helps you ask better questions and pick a recovery partner that protects your accounts and your reputation.

How AI Is Entering the Debt Collection and Recovery Space

Predictive Analytics and Account Prioritization

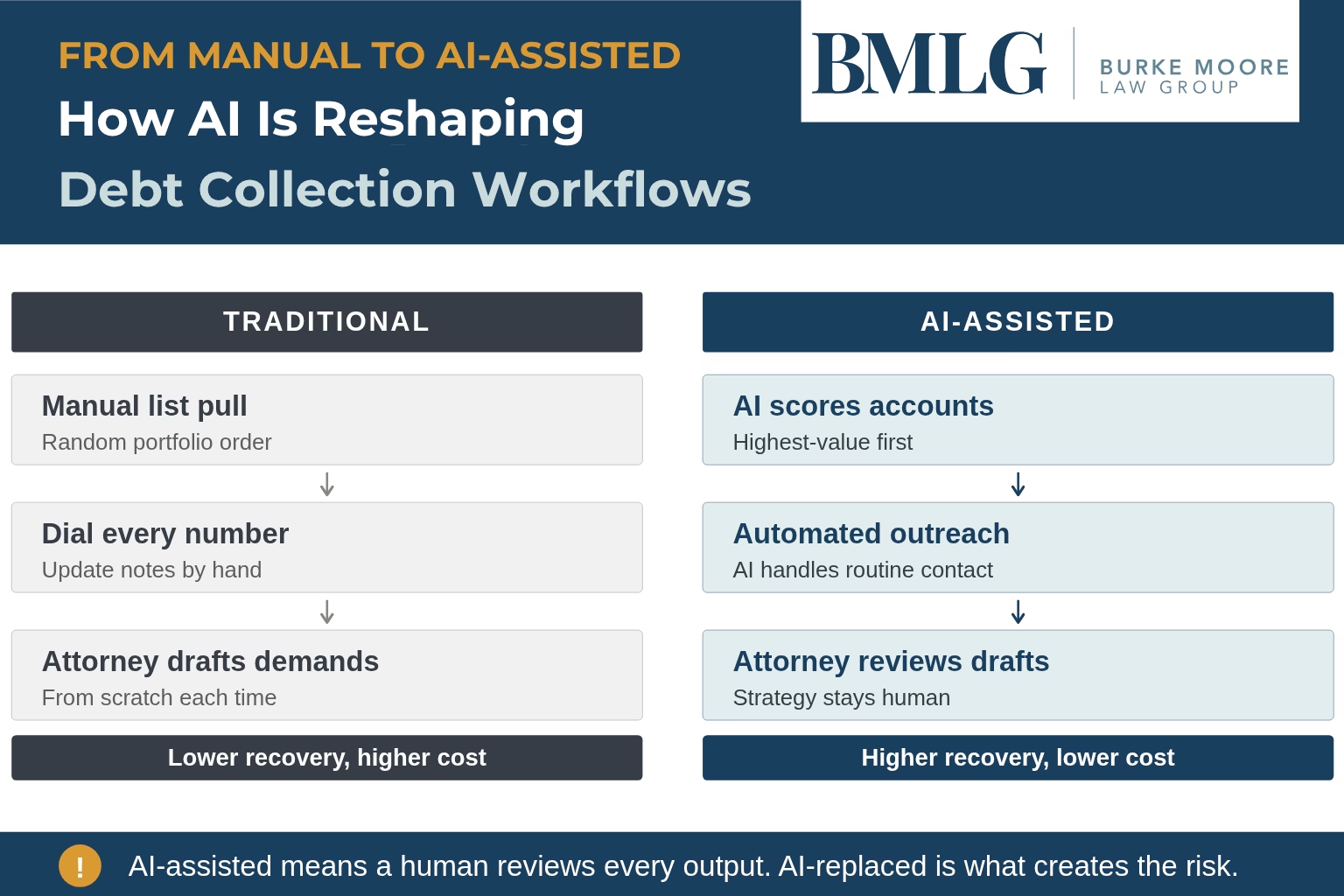

AI tools score delinquent accounts by likelihood of recovery, using historical data and machine learning to flag which files deserve attention first. Debt collectors and attorneys can then work the highest-value, most recoverable accounts instead of churning through a portfolio top to bottom. The payoff is a higher recovery rate at lower operational cost.

Automated Outreach and Right-Party Contact

AI-powered systems can now handle most of the repetitive parts of collections: payment reminders, dispute intake, and right-party contact verification. AI agents can place phone calls, route consumers to a payment portal, and offer payment plans through digital channels so human agents can stay focused on negotiations, settlements, and the complex cases that actually need a person on the line.

From Manual Workflows to AI-Assisted Processes

Traditional methods relied heavily on manual tasks: pulling lists, dialing every number, and updating notes by hand. AI in debt collection now compresses those manual workflows into faster, more accurate processes. Fintech lenders, banks, and third-party debt collectors are all moving toward AI-assisted models for the same reason: better operational efficiency, fewer human errors, and improved customer experience for consumers who want to resolve their debt.

Why Law Firms Are Building Formal AI Policies

The legal industry has watched a wave of AI-related court errors over the past two years, and the response from bar associations and courts has accelerated. Firms without clear AI policies are exposing themselves and their clients to potential risks. Ongoing training for attorneys and staff helps AI-generated outputs meet ethical obligations and professional standards.

Court Errors Are Showing Up at Every Level

Federal and state courts have documented dozens of cases where attorneys filed briefs containing fake citations generated by AI. Sanctions, fee awards, and disciplinary referrals have followed. The risk of an AI-generated error reaching a judge is no longer theoretical, and the legal industry is reacting accordingly. Firms now run regular training so attorneys and staff understand both the power and the limitations of AI tools.

Bar Associations Are Stepping In

The American Bar Association issued its first formal ethics opinion on generative AI in 2024, addressing client confidentiality, competence, and supervision. State bars across the country are following with their own ethical guidelines, disclosure requirements, and practical guidance for AI use in legal practice.

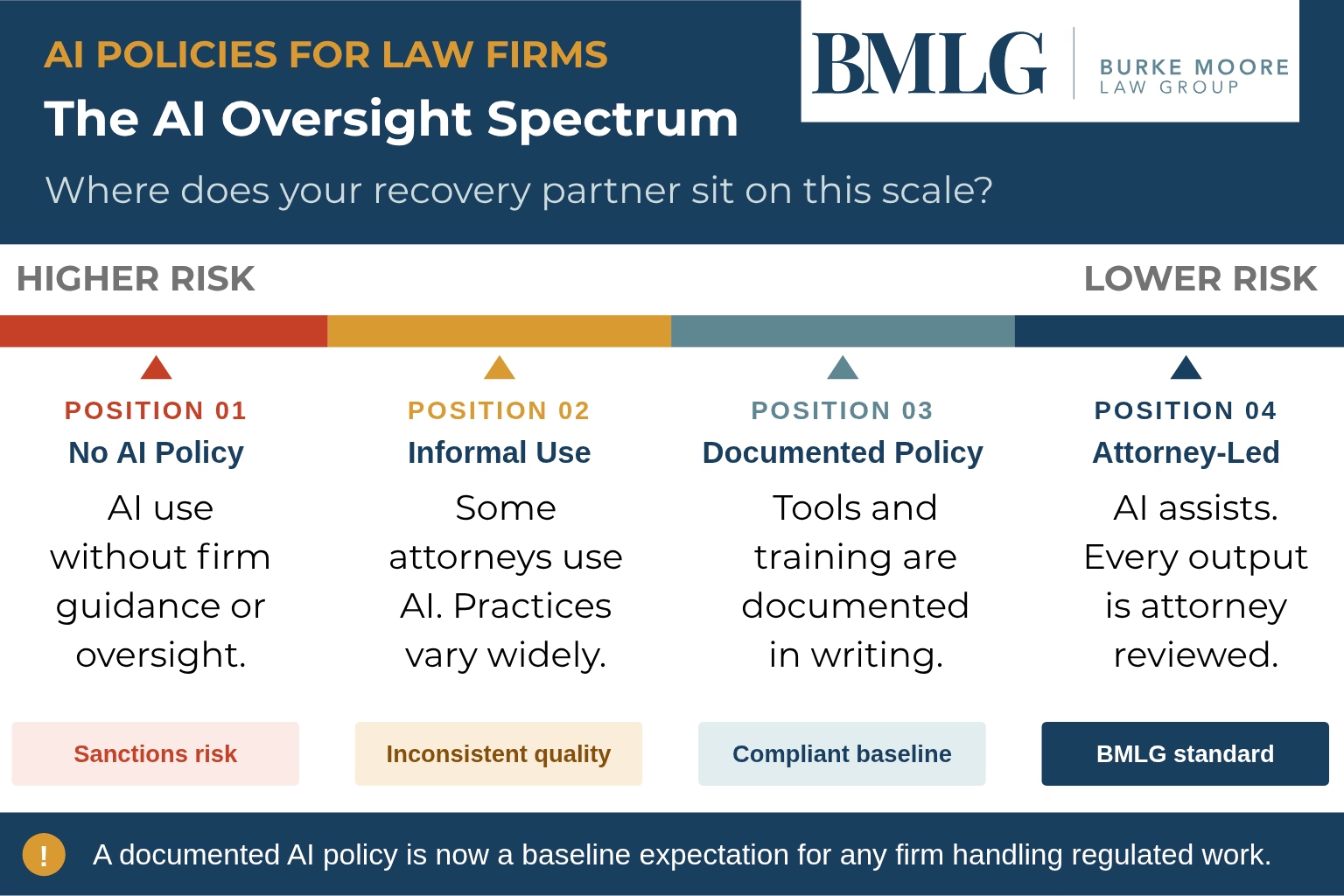

Firms Without Policies Are Creating Liability

A law firm without clear guidelines on the use of AI is exposing itself and its clients to real risk. Sensitive client information can leak through unsecured AI tools, AI-generated outputs can include hallucinated case law, and AI-generated content filed without human oversight can violate professional standards. A documented AI policy is now a baseline expectation for any firm handling regulated work.

What Responsible AI Policy Looks Like in a Creditors’ Rights Firm

A responsible AI policy at a creditors’ rights firm separates the work AI does well from the work that still belongs to a licensed legal professional. AI tools should be used to assist attorneys, not replace them, especially in legal strategy areas such as negotiations and settlement decisions. AI-assisted processes can help reduce operational costs, but attorney judgment still drives final decisions.

Where AI Adds Value

| Function | How AI helps |

| Account prioritization | Scoring delinquent accounts by likelihood of recovery |

| Compliance monitoring | Flagging communications that fall outside Reg F or state law |

| Workflow efficiency | Reducing routine tasks like document indexing and data entry |

| Documentation | Generating first-draft demand letters and status reports |

| Customer interaction | Answering routine status questions through self-service portals |

Where Attorney Judgment Remains the Standard

Legal strategy, settlement negotiation, courtroom litigation, judgment enforcement, and bankruptcy matters require attorney experience and discretion. No AI system can replicate the practiced judgment of a licensed legal professional reading a case file, weighing the practical legal solutions, and negotiating with opposing counsel on a contested account.

AI-Assisted, Not AI-Replaced

AI can increase operational efficiency and assist attorneys, but it cannot replace them. AI-assisted means a human reviews every output before it leaves the firm. AI-replaced means an automated system filed a motion, sent a demand letter, or settled an account without an attorney signing off. The first model lowers cost while protecting your portfolio. The second can void judgments, trigger disciplinary action, and put your recovery program at risk.

What This Means for Creditors Choosing a Recovery Partner

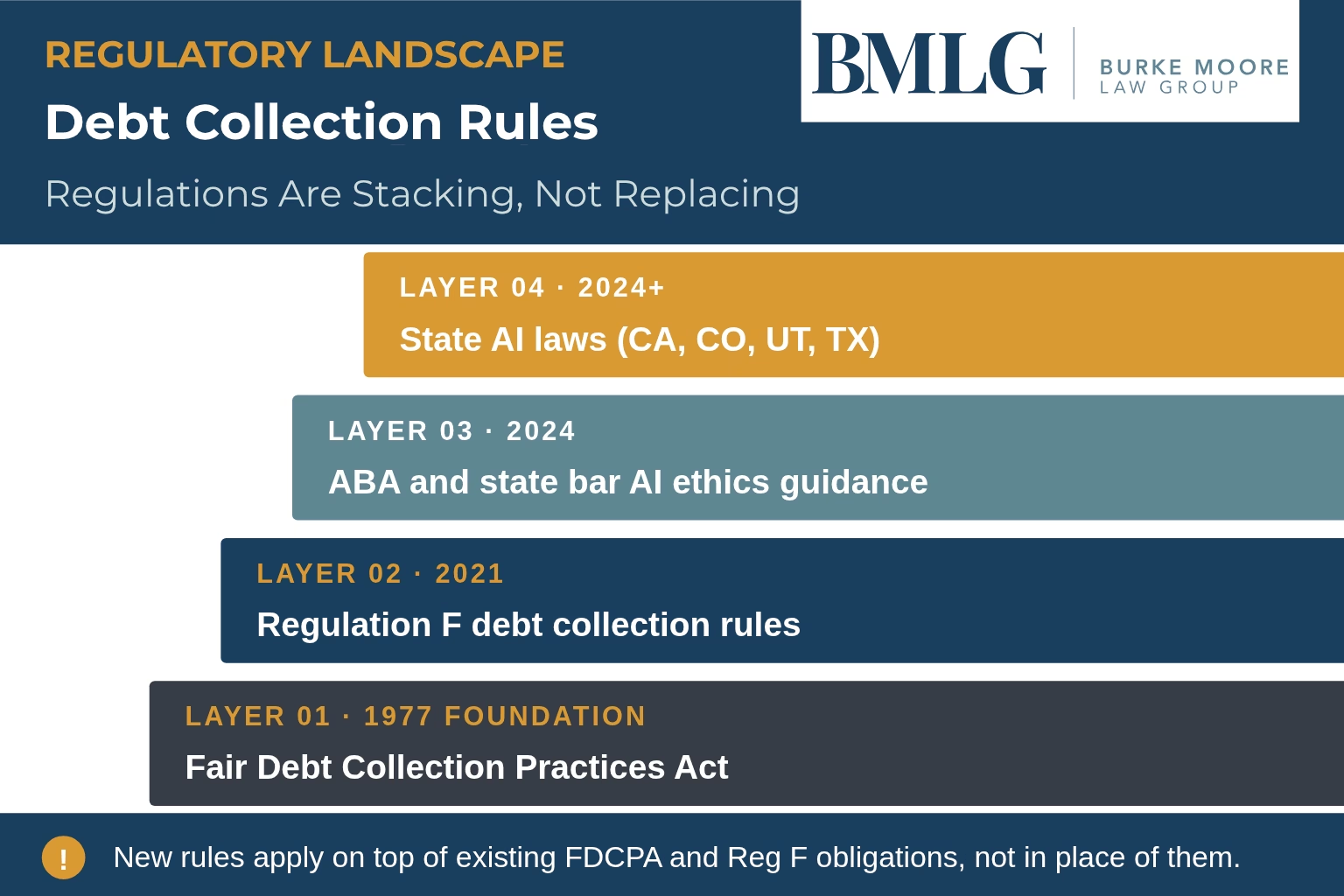

Compliance Risk Under FDCPA, Reg F, and State Law

The Fair Debt Collection Practices Act, Regulation F, and a growing list of state consumer protection statutes set strict requirements for how debt collectors communicate with consumers. AI adoption without attorney oversight can produce communications that violate these regulatory requirements, creating exposure for the original creditor as well as the firm.

Technology Supporting an Attorney-Led Process

The strongest models play to each side’s strengths. AI handles intake, account prioritization, compliance review, document generation, and reporting. Attorneys handle legal strategy, court filings, and settlement decisions. The result is a faster, cheaper recovery process that still holds up in court.

Questions Creditors Should Be Asking

Before placing accounts with any debt collection firm, ask:

- How is AI used in your practice, and which AI tools have you approved?

- Who reviews AI-assisted work product before it leaves the firm?

- How do you document compliance with Reg F and state regulatory requirements?

- What controls protect member or customer nonpublic personal information?

- How do you handle data privacy and data security when AI systems touch confidential information?

Good answers will be specific. Vague answers are a warning sign.

A Regulatory Landscape Worth Watching

AI regulation in the legal and collections space is still developing. Creditors should monitor it actively rather than wait for a final framework.

Federal and State AI Rules Are Still Developing

Federal regulators have not finalized broad AI rules for financial services or the legal industry, but the direction is clear. Disclosure, human oversight, and risk management documentation are showing up in proposed and final guidance across multiple agencies.

State AI Laws Are Layering on Top of Existing Rules

States including California, Colorado, Utah, and Texas have passed or proposed AI laws affecting algorithmic decisions, dispute resolution, and disclosure of generative artificial intelligence in customer interactions. These rules apply on top of existing FDCPA and Reg F obligations, not in place of them.

Move Now, Not Later

Creditors should partner with counsel that already operates under documented AI policies and clear compliance protocols. Firms that are getting ahead of this now are building the kind of risk management posture that holds up under audit, examination, or litigation.

AI Is a Double-Edged Sword

AI Ethics and Laws for Balancing Artificial Intelligence (AI) and Safety. Developing AI codes of ethics. Compliance, regulation, standard , business policy and responsibility for privacy data.

AI tools are not exclusively available to creditors. Consumers, members, and customers are using free and low-cost AI tools to draft disputes, generate complaint letters, and respond to collection activity. This makes the average consumer far more capable of challenging a debt, driving up contestation and litigation — and ultimately, creditor attorney fees. That trend will only grow as AI technology becomes cheaper and more accessible.

What That Means for Creditors

- More regulatory complaints filed by consumers using AI-generated templates

- More counterclaims and responsive litigants in routine collection suits

- More active motion practice on accounts that used to settle quickly

- Higher per-account legal costs across the collection process

How Prepared Creditors Respond

Smart creditors are getting ahead of this:

- Establish protocols for triaging and responding to AI-generated disputes and complaints

- Retain experienced counsel capable of handling both routine recovery and contested litigation

- Address fee arrangements for contested matters within representation agreements

- Deploy AI solutions internally to free up staff time for higher-value accounts

The creditors that prepare now will hold the competitive advantage when AI-generated consumer activity reaches its peak.

Final Thoughts

AI is reshaping how the legal profession works, and debt collection is not insulated from that shift. Predictive analytics, AI agents, and machine learning are already reducing operational costs and improving customer satisfaction across financial services. At the same time, courts and bar associations are setting ethical standards for how attorneys use AI in legal work. For creditors, the question is no longer if your recovery partner uses AI. The question is if they use it responsibly, under proper attorney supervision, and within industry standards that protect your portfolio and your customers.

Burke Moore Law Group combines attorney-led debt collection, bankruptcy, and claims recovery with documented technology controls and clear AI compliance protocols.

Contact our team to talk through a recovery strategy built on attorney-led expertise.